Client

The medium and long-term line maintains long-term thinking. USDA said that the global 2016/17 sugar market supply gap is expected to narrow to 4.3 million tons, and the 2015/16 supply gap is estimated at 6.9 million tons. The sales data in September showed a general performance. As of the end of September, the national sugar inventory was about 860,000 tons (different from the total number of sugar associations), and the national transfer settlement decreased slightly. Mid- and long-term maintenance of slow cattle ideas, sr1701

Concerned about the buying opportunities after the callback, the current price suggests to continue to hold more than the previous period, you can consider the relevant report to establish a long position on the 1705 bargain.

Core point

Two sources involved in the national sugar store auction said that in the first auction in the past five years last Friday, the transaction price was 15% higher than the government's bidding reserve price (6,000 yuan / ton), and buyers' demand was strong. .

Sugar yield

Stocking sugar consumption before the Spring Festival

Investment targets

Source: CIC Futures Research Institute

1. Market overview

USDA said that the global 2016/17 sugar market supply gap is expected to narrow to 4.3 million tons, and the 2015/16 supply gap is estimated at 6.9 million tons. According to the US Department of Agriculture, China's sugar imports will be a record 7.9 million tons, with total consumption increasing by 1.7% to 17.8 million tons, a record high. USDA added that China's sugar production will fall by 2.3% to 8.2 million tons in 2016/17 (starting on October 1). According to the US Department of Agriculture, sugar consumption in India is expected to increase to a record 17.2 million tons, an increase of 1.5% over the current year. The country's sugar production may fall by 7.9% to 25.5 million tons. Despite this, Brazilian sugar production is expected to increase by 7% to a record 37.1 million tons, which will help cut the supply gap.

Brazil: Data from the Brazilian Union of Sugarcane Industries (Unica) in São Paulo, Brazil, showed that sugar production in central and southern Brazil was 2.83 million tons in the first half of July, up from 2.79 million tons in the second half of June. In the first half of July, sugar cane crushing in sugar mills in central and southern Brazil was 46.74 million tons, down from 47.89 million tons in the second half of June. Earlier, Kingsman's survey of analysts showed that sugar cane crush was 14.62 million tons and sugar production was 2.86 million tons in the first half of July in central and southern Brazil.

India: Affected by the continuous drought, India has cut production significantly. India is the world's second-largest sugar producer and the largest consumer of sugar. Its sugar production reached a high of 28.03 million tons in the 2014/15 crop season, which is the fifth consecutive year of overproduction. Later, due to the drought caused by the strongest El Niño phenomenon in history, domestic sugar production in the 2015/16 crop season fell by 11% year-on-year to 25 million tons. It is expected that the 2016/17 crop sugar production will continue to decline.

Thailand: Indonesia's sugar production in 2015/16 is expected to be 2.3 million tons, compared with 2.1 million tons in 2016/17.

China: In 2016/17, China's sugar planting area reached 1,433 thousand hectares, which was basically the same as last year.

Recently, there are more rainwater in the northern sugar beet production area, which is conducive to the growth of sugar beet. The sweet menu production is expected to increase by 0.75 tons per hectare in the previous year. The rainwater in Guangxi and Yunnan sugarcane areas is more than low temperature, and the number of sugarcane seedlings and plant height are down. It is estimated that the yield of sugarcane in China in 2016/17 will be reduced by 0.75 tons per hectare in the previous year. The sugar production rate will increase in 2016/17. It is estimated that China's sugar production will reach 9.9 million tons in 2016/17, an increase of 1.2 million tons from the previous year.

On the whole, in 2016, the international sugar market will face a shortage. The international sugar market is expected to have a gap, and we will keep a lot of ideas in the future. Domestic sugar production is expected to increase by 1 million tons in the next crop season. The overall supply of domestic sugar is loose. The national reserve sugar stock is about 5.6 million tons.

2. Analysis of supply and demand fundamentals

2.1 Analysis of China's supply and demand

Chart 1 domestic sugar supply and demand balance sheet

Source: Wind, CIC Futures Research Institute

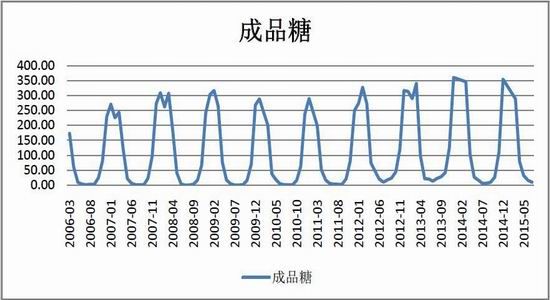

Chart 2 monthly finished sugar consumption (monthly)

Source: Wind, CIC Futures Research Institute

Chart 3 carbonated beverage production (monthly)

Source: Wind, CIC Futures Research Institute

It can be observed from Figures 2 and 3 that the consumption of carbonated beverages and finished sugar is gradually increasing, but the growth has been slow in recent years, which also proves that it is difficult to increase the total consumption of sugar in China. The total domestic consumption of sugar has a large relationship with the population base. The total national consumption is about 15 million tons, and we believe that domestic sugar consumption will maintain a slow growth pattern. The annual growth is expected to be about 5%.

In summary, consumption has not had a bright spot and maintained steady growth. It is estimated that the 2016/2017 crop season will produce 9 million tons of sugar in China, and the output will increase slightly. The spot is biased towards the bulls.

3. Market analysis

3.1 Market focus changes

In the 16/17 season of Yunnan, sugar cane was priced at 420, and the linked sugar price was 5,800, which was flat year-on-year. In the 2016/17 crop season, the purchase price of sugarcane in Guangxi is expected to increase to 480 yuan / ton. As shown in the table below, according to the purchase price of sugarcane 480 yuan / ton, 4.5 tons per mu, the net income per mus of sugar cane is about 652 yuan. If the new plant sugar cane subsidy given by the sugar factory is added, the net income per mu can reach 700 yuan. the above.

The second thing to pay attention to is the transaction situation of the state reserve and the degree of market recognition. In the past years, the more you went up, the more you judged the market mentality based on actual transactions.

3.2 Price changes

Chart 4 imported sugar price

Source: Wind, CIC Futures Research Institute

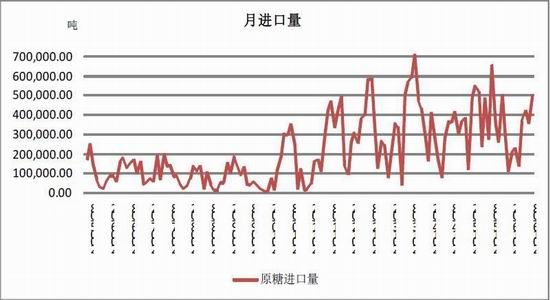

According to data provided by the China Customs Statistics Institute on October 24, China imported 497,500 tons of sugar in September 2016, a decrease of 24.19% from September of last year, but higher than the import volume in August this year (3,630,300 tons in August). In July, imports were 419,300 tons, imports were 369,200 tons in June, imports were 135,500 tons in May, imports were 225,300 tons in April, imports were 209,600 tons in March, and imports were 107,200 tons in February.

Due to the slight decline in international sugar prices, the average import price of sugar in China in September 2016 was US$361.15/ton, slightly lower than the average import price in August (the average import price in August was US$365.79/ton).

In the first nine months of 2016, China imported a total of 2.162 million tons of sugar, a decrease of 29.95% over the previous year.

Chart 5 white sugar futures price yuan / ton

Source: Wind, CIC Futures Research Institute

3.3 Position changes and technical analysis

Chart 6 US raw sugar positions

Source: Wind, CIC Futures Research Institute

As of November 18, the non-commercial long position of US Sugar No. 11 was 294,727 lots, and the non-commercial short position was 41,822 lots. The speculative position is a net long position. From the perspective of positions, speculatively profited and left, and staged highs appeared. However, the tone of the rise will remain unchanged and the rate of increase will slow down.

Chart 7 white sugar technical analysis chart

Source: CIC Futures Research Institute, Master Bo Yi

From a morphological point of view, white sugar broke through the previous high point and is currently in the side of the lower rail of Brin, in a sideways position. As long as the future does not fall below the lower track, more than one can always hold.

3.4 domestic spot market

Chart 8 basis is at a normal level

Source: Wind, CIC Futures Research Institute

The basis is currently at -137, the last period -119, the spot price price is slightly adjusted, the futures price is fast spot price, the domestic spot is relatively strong, and the futures price remains strong.

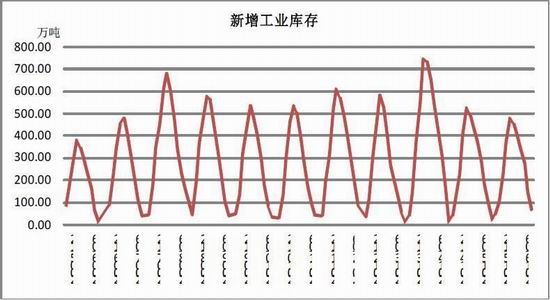

Chart 9 National New Industrial Stock

Source: Wind, CIC Futures Research Institute

By the end of May, the national industrial inventory of new sugar was 4,044,300 tons, which was more consistent with previous years. At a relatively low level.

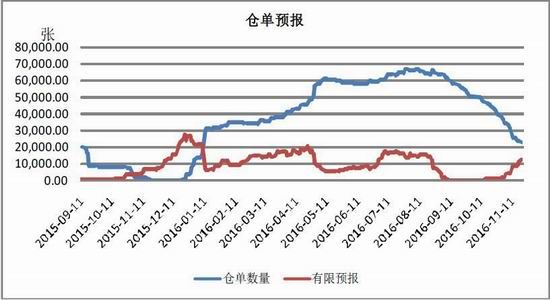

Chart 10 Zhengshang's white sugar warehouse receipt forecast

Source: Wind, CIC Futures Research Institute

Chart November import volume

Source: Wind, CIC Futures Research Institute

Imports in January-July decreased by 37% year-on-year, and the gap between domestic and foreign sugar prices narrowed, and the market supply was sufficient.

Chart 12 national sales rate

Source: Wind, CIC Futures Research Institute

3.4 Industrial ethanol

UniCA's latest biweekly data show that by the end of October, Brazil's central and southern Brazil had a total of 537 million tons of sugar cane, up 4.25 billion tons from the previous season. The sugar production was 32.68 million tons, up 16.64% from the previous season. The sugar yield was 13.41%, up 0.31% year-on-year; the ethanol production was 22.572 billion liters, down 4.19% from the previous season's last season, 23.560 billion liters, of which the hydrous ethanol was 13.24 billion liters, down 11.11% year-on-year, and the absolute ethanol was 9.548 billion liters. 7.18%. In the second half of October, the import of sugar cane was 31.73 million tons, down by 17.87% from the previous season, and the production of sugar was 2.049%. The sugar production was 209,900 tons, which was 6.00% lower than the previous season's 2.18 million tons. The sugar yield was 13.74%, down 2.20% year-on-year. Ethanol production was 1.303 billion liters, down 29.33% from the previous season's 1.844 billion liters, of which 678 million liters of hydrous ethanol, down 36.25% year-on-year, and 625 million liters of anhydrous ethanol, down 19.91% year-on-year.

More sugar cane is used to produce raw sugar, and the sugar production ratio is increased.

Ethanol production declined, and crude oil is expected to maintain a volatile trend in the later period. In the case of expected decline in ethanol production, the latter price is relatively firm.

4. Analysis of logical conduction and influence market factors

4.1 Wave Logic

Long-term influencing factors are mainly in supply and demand changes, based on changes in agricultural weather cycles and macroeconomic cycles.

Short-term influencing factors The price of domestic new sugar prices, the trend of foreign sugar prices, and the speculative rate of domestic funds. In the medium and long term, the future is in the sugar production cycle, and the market continues to speculate on the supply gap. It is reported that the 2016/17 crop season is expected to increase the sugarcane purchase price in Guangxi to 480 yuan/ton. Sugar production costs are expected to increase. The price trend of white sugar mainly depends on supply, the demand is relatively rigid, and the impact on price is small.

4.2 Domestic planting area increased slightly

According to the survey data, the sugarcane planting area has increased slightly. The weather is better this year. It is expected that the sugar yield will be higher. The sugar production in this quarter will be 10 million tons, an increase of 1 million tons from the previous quarter.

4.3 The spot market is abundantly supplied

The domestic spot price is relatively firm, and many companies are optimistic about the future sugar price. Foreign spot prices have continued to rise due to weather disasters. At the same time, domestic consumption has not improved significantly. As the output of sugar in the new crop season is expected to increase slightly, the market supply is still relatively abundant. Spot sales are clearly under-represented at high prices.

4.4 The medium and long-term sugar market will gradually become stronger due to the impact of production reduction

In 2016, the international sugar market will face a shortage. 2016/17 analyst firm PlattsKingsman raised the global sugar supply shortage forecast for 2016/17 by 570,000 tons to 6.45 million tons. This year, the world is affected by the weather and production is expected to decline. Estimates for global sugar market supply shortages are quite different, but most believe that the shortage in the next two years is 4-8 million tons. Expectations for a global supply shortage in the sugar market have pushed sugar prices up in 2017.

5. Market outlook and investment advice

5.1 Unilateral Trading: Maintaining Slow Cow Thinking

The National Development and Reform Commission said on the 30th that in order to ensure the stable supply of sugar and the stable operation of the price, the Development and Reform Commission, the Ministry of Commerce and the Ministry of Finance decided to launch the first batch of national reserve sugar in the second half of October, with a quantity of 350,000 tons and a bidding reserve price of 6,000 yuan. / ton (warehouse delivery price). The national reserve sugar was put into public auction through the electronic network system of the China Merchants Reserve Commodity Management Center, and the bidding unit was 300 tons.

Since the domestic sugar production cost is about 5,400, the late price center should be above 5400. USDA said that the global 2016/17 sugar market supply gap is expected to narrow to 4.3 million tons, and the 2015/16 supply gap is estimated at 6.9 million tons.

Overall, in the future, domestic sugar supply and demand balance, the total demand is about 15 million tons, and the total supply is about 18 million tons. There is a gap in foreign sugar, and ethanol production is declining. It is expected to maintain a strong trend in the later stage and is expected to break through the 7000 mark. Before the new cropping season, the sugar factory inventory continued to decline, the sugar factory pressure was small; the outer disk was high, the smuggling decreased, and the sugar price was supported; the climate uncertainty increased, and the climate speculation space was large. However, the new crop season is expected to increase production, and the country will save money after the price of sugar rises. At the same time, the smuggling of hidden dangers has existed for a long time, which has inhibited the sharp rise in sugar prices.

As both domestic and domestic are in the bull market cycle of the sugar market, future increases are a high probability event. In operation, the mid- and long-term maintenance of slow cattle ideas, sr1705 concerned about the buying opportunities after the callback, it is recommended to continue to hold more than the previous period.

CIC Futures Lu Shiqiang

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Super Soft Poluester Sock,Super Soft Socks,New Poluester Socks,Super Soft Cozy Home Socks

Jingjiang Pingdong Import&Export Co.,Ltd , https://www.jingjiangsocks.com