Client

On the international front: the bull market may be coming to an end, and India has not responded to the tariff issue, which is not good for the bulls.

Domestic aspects: From the past experience, the end of the Spring Festival to May is the off-season of consumption, and the domestic sugar price is gradually weakening.

In terms of policy: the price of dumping has gradually declined, and the market is not optimistic about the market outlook. There are still many cards that can be played.

First, the fundamental analysis

White sugar has been in the bull market and reached its peak in the second half of 2016, with the highest increase of more than 30%. Under the background that the fundamentals of white sugar are not completely good, the rate of increase is amazing. Time went into February, Zheng sugar has experienced a long-lasting shock and has not been able to decide the direction. The main producing areas in Guangxi have begun to squeeze. By February 23, seven sugar factories have completed the mission of this season, and more than 20 pre-finished work will be completed by the end of February. In March, the number of sugar mills will reach a peak, and the new sugar supply will also enter a peak period. At present, the weather conditions in the main producing areas are good and suitable for harvesting. It is expected that the sugar factory will complete the crushing task ahead of previous years, and the supply pressure of new sugar listing will be advanced. Domestic new sugar is expected to increase in the 16/17 season

According to the data provided by the Sugar Association, as of the end of January, the total sugar production in the country reached 4,539,600 tons, an increase of 330,000 tons over the same period, the sales of sugar reached 1,934,200 tons, and the sales rate reached 42.7%. Today's high sugar prices have made sugar mills and sugarcane farmers taste the sweetness, and the expansion of the planting area in the next season is unquestionable. At present, the major sugar factories are producing at full capacity: the main producing areas in Xinjiang have completed all the crushing, with a sugar production of 480,000 tons. The Hainan Yinzhou area has also completed the harvesting. Most of the sugar factories in Guangxi are still being squeezed and reach the peak of production. At present, there are light rains in the Guangxi area and the soil is wet, which is conducive to the sowing of new planting sugarcane and the growth and sprouting of the cane. As the speed of new sugar listings accelerated, investors began to pay attention to later consumption. Judging from the historical law, Zheng sugar entered the low season after the Spring Festival and continued until the end of May. During this period, the price of sugar was easy to fall.

Figure 1: Domestic sugar supply and demand balance table unit: thousand tons

Source: US Department of Agriculture

The cost of sugar in the new season is about 5800 yuan.

According to the purchase price of 380 yuan/ton of sugarcane in the 16/17 season in Guangxi, the corresponding total cost of sugar-containing tax is about 5,800 yuan. The sugar-making sugar cost is generally the bottom of the late-price operation, giving the sugar price a certain support. However, everything is not absolute. In the 12/13 season, there have been cases where the price of sugar has repeatedly tested the production cost, and the collapse has finally broken through the “cost base†into the big bear market. Therefore, production costs can be used as a primary reference for the bottom to provide a reference, but not absolute. Imports have no signs of relaxation

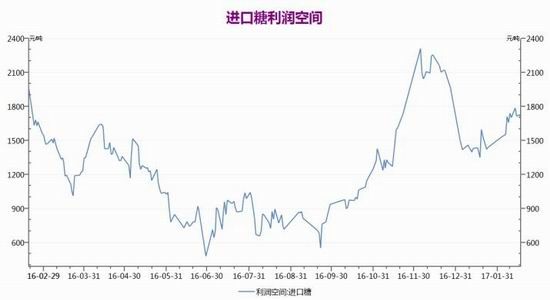

According to the import data released by the customs, as of the end of December, the cumulative import of the 2016/17 cropping season was 866,600 tons, a decrease of 539,300 tons compared with the same period of last year, showing a trend of improvement. One of the reasons is that the state strictly controls imports and tries to increase trade tariffs to further control the amount of imports in the later period. On the other hand, the international sugar prices are high and the import costs are increased. Many traders have suspended imports. At present, the import of Brazilian sugar in the quota is 5,250 yuan, and the additional import price is 6,726 yuan, which is already at the recent high level. However, at the time of the downward adjustment of international sugar prices, domestic import sugar merchants saw profits. In January, the import volume reached 410,000 tons, a record high in recent months. In the later period, international sugar prices will be adjusted downwards, and import profits may further increase. According to the ship report published by Williams Shipping Company, 42,000 tons of raw sugar has been sent from Brazil port to China in February and is expected to arrive in Hong Kong in March.

Figure 2: Imported sugar profit space unit: yuan / ton

Source: Wind, Cinda Futures R&D Center

Figure 3: Sugar import unit: ton

Source: Wind, Cinda Futures R&D Center

The National Reserve began to play cards one after another, and the price of the reserve was lower.

In the new cropping season, the state has dumped reserves five times, and its reserves are 200,000 tons, 108,000 tons, 92,000 tons, 92,000 tons and 249,300 tons, respectively, but the average price of storage is all the way down, respectively 6850 Yuan, 6,850 yuan, 6,725 yuan, 6,725 yuan and 6,261 yuan. After the first few deposits, the average transaction price was relatively high, which proves that the market is still optimistic about the later stage of the sugar market. However, the average price of stocks on Monday fell directly to around 6200, which proved that the market is not optimistic about the price of sugar in the later period. At present, the spot price in the market is basically around 6,700. The price of the dumping is nearly 500 yuan/ton than the spot price. Of course, there are factors such as slightly poor quality of the national reserve, but in the final analysis, the market is beginning to be rational, and the supply is large in the later stage. In the case of an increase, the National Reserve Sugar began to return to the normal price range.

In addition, the country’s tradition of changing 400,000 tons of Cuban sugar directly into the national treasury this year has become a model for selling in Hong Kong. This has also put some pressure on the market. It can be foreseen that the sugar supply in the later market is mainly concentrated on the five aspects of new sugar, national sugar, Cuban sugar, imported sugar and smuggled sugar. The impact of the national sugar dump on the decline of sugar prices in the later period. The power will be deeply reflected. International sugar market bull market may be coming to an end

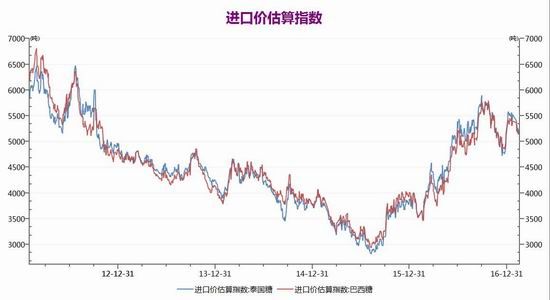

At present, the focus of the international market is concentrated in India: India suffered a reduction in production during the crop season. USDA expects its sugar production to be approximately 23.95 million tons, a year-on-year decrease of 13.02%. At the same time, India is a major consumer, with an estimated 16/17 squeeze. In the quarter, its consumption increased by about 2% year-on-year to 24.5 million tons. The short supply and demand gap caused supply and demand, and also promoted import demand. The market expects India to import 1.5 million tons of raw sugar and cancel import tariffs in this season, which is to stimulate raw sugar. An important factor, but the Indian government has not responded to the tariff issue. In Thailand, production has also been reduced in this season, and it is expected to produce 9.27 million tons of sugar. Overall, the reduction in production in India and Thailand has led to a global supply shortage of nearly 3.363 million tons in this crop season. In addition, the Middle East region's Ramadan this year ahead of the end of May, leading to the demand for the international market in advance, the demand for sugar prices are easy to rise and fall.

However, it is expected that the next crop season will reverse. Many research institutes expect oversupply in the 17/18 crop season: First, Thailand will expand the planting area and further increase the area of ​​new planted sugarcane. Second, Brazil still produces sugar. Large amount, in the context of high raw sugar prices, sugar mills are more inclined to increase sugar alcohol production than sugar; Finally, Brazil's January precipitation is sufficient, sugarcane growth will be better than the same period last year, south central Brazil The production of sugarcane in the region will hit a record high. On the whole, the previous bull market feast will come to an end.

Figure 4: Estimated import price index unit: yuan / ton

Source: Wind, Cinda Futures R&D Center

Second, operational recommendations

Operational recommendations: At present, the strength of domestic sugar prices is mainly due to the high international sugar prices that inhibit imports and smuggling, coupled with capital speculation, the sugar market's bull market was established. The focus of later attention is mainly on three aspects, namely, imports, national reserves and new sugar production. Although the price of sugar is still high, but mid- and long-term investors can properly place empty orders at high levels. After all, the bull market has reached the end, it is time to change the way of thinking about the sugar market in 2017 with a rational mindset. The international raw sugar season will be reversed, and there will be an oversupply again. The bull market feast will come to an end. With the end of the international sugar market, the domestic sugar market has also been affected. As the production cycle reappears, sugar prices will fall.

Cinda Futures Zhang Xiufeng

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Yangzhou Lansun Slipper Co.,Ltd , https://www.lansunhospitality.com